The Invisible Crisis:

How Hormuz Is Strangling the Chip Industry

The world is watching oil. It should be watching helium. Qatar’s Ras Laffan shutdown has removed a third of global helium supply — and the consequences for semiconductor manufacturing, AI hardware, and the entire chip ecosystem are only now becoming clear.

What Nobody Is Talking About

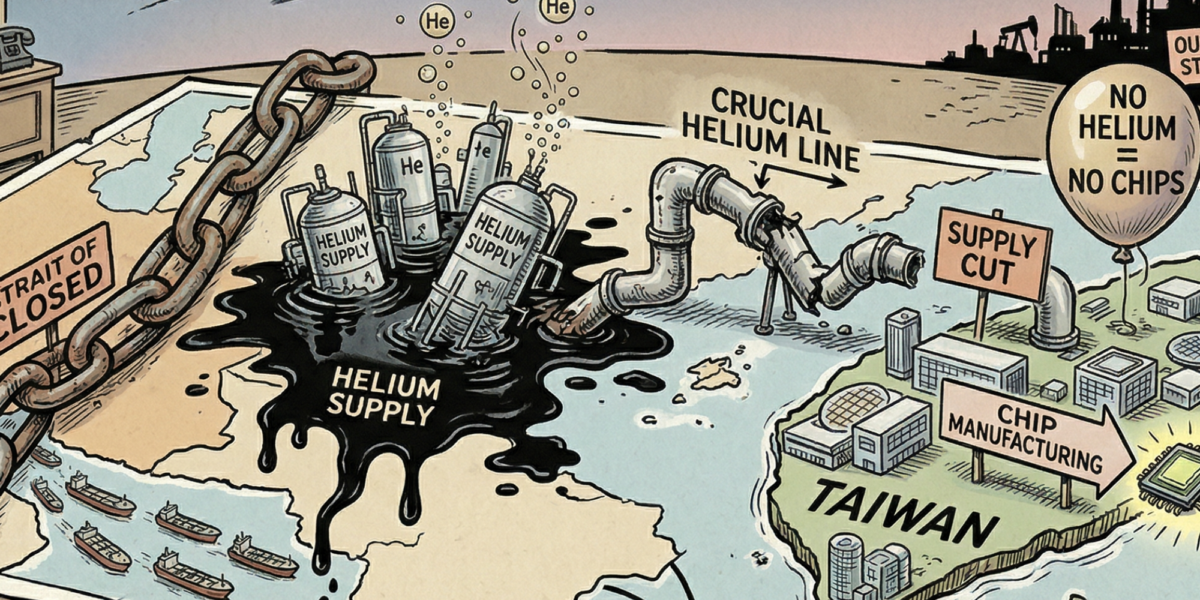

Every barrel of oil that cannot pass through the Strait of Hormuz gets counted. Every tanker stranded in the Persian Gulf, every force majeure declaration from Kuwait or Qatar, every drone intercepted over Shaybah — these make headlines and move markets in real time. But there is a second shock running underneath all of it, slower, less visible, and in some ways more structurally dangerous. It is the helium shock.

Helium is not a byproduct of oil. It is a byproduct of natural gas processing — specifically, of the liquefaction that produces LNG. This is why the attack on Qatar’s Ras Laffan industrial complex on March 2, 2026 did not just remove 20% of global LNG supply from the market. It simultaneously removed roughly a third of global helium supply. The two commodities are physically co-produced at the same facility. When Ras Laffan goes offline, helium goes offline with it.

The world has known for years that the Strait of Hormuz is a chokepoint for oil. What it has not properly reckoned with is that the same geography — the same 33 kilometres of water between Iran and Oman — is also a chokepoint for the gas that manufactures its microchips, cools its hospital scanners, and pressurises its rockets. The closure of Hormuz is not one supply shock. It is several, stacked on top of each other, each with its own timeline and its own industrial cascade.

The Gas That Cannot Be Replaced

Helium is the second lightest element in the universe and the most chemically inert gas known to science. These two properties, combined, make it irreplaceable in a remarkable range of industrial and medical applications. Nothing else combines an extremely low boiling point of 4.2 Kelvin, chemical inertness, high thermal conductivity, and non-flammability at industrial scale. Every candidate substitute fails on at least one of these dimensions.

How helium functions in semiconductor manufacturing

In chip fabrication, helium performs three distinct functions at different stages of the wafer manufacturing process. During plasma etching, helium is injected between the wafer and the electrostatic chuck to dissipate intense heat before the wafer warps. In photolithography — particularly EUV at 13.5-nanometre wavelengths — helium creates the stable vacuum environment that keeps contamination at zero. And in leak detection, its small atomic size allows it to penetrate microscopic gaps that would stop any other gas, making it the only viable method for testing the hermetic integrity of vacuum chambers. Critically, as chip geometries shrink and EUV adoption accelerates, per-wafer helium consumption is actually increasing. The industry’s trajectory is toward more helium per chip, not less.

Nitrogen and argon can replace helium in some peripheral industrial applications. They cannot replace it in EUV cooling, wafer chuck heat transfer, or leak detection. Hydrogen is reactive. Neon lacks thermal conductivity. This is not a hedged technical position. It is a physical constraint that has been understood for decades and acted upon almost nowhere.

Beyond chips: the full exposure map

Semiconductor manufacturing accounts for roughly 21–25% of global helium demand — the single largest industrial consumer. MRI scanners account for approximately 19%: liquid helium cools the superconducting magnets that make MRI technology function, and without it more than 14,000 machines worldwide become, in the words of one safety consultant, “very expensive paperweights.” Aerospace uses helium to pressurise rocket fuel tanks and purge propulsion systems. India, China, and South Korea — all running ambitious space programmes — depend on stable supply. CERN’s Large Hadron Collider runs on helium cryogenics. Demand is projected to roughly double by 2035 as AI manufacturing expands and space investment grows. The current crisis is striking a market that was already tightening before the first drone reached Ras Laffan.

A Market Built on Four Suppliers — One Now Gone

Global helium production is extraordinarily concentrated. The United States produces approximately 81 million cubic metres annually. Qatar, at full capacity, produced roughly 63 million cubic metres in 2025. Algeria and Russia contribute around 8% each. Four countries; four vulnerabilities. The charts above show the structural picture. What they cannot convey is how quickly effective supply narrows when you apply the filters that matter in a crisis.

Sanctions rules out Russia. Distance rules out rapid rerouting — helium is transported as a cryogenic liquid in specialised ISO containers, and routing around the Cape of Good Hope adds approximately 3,500 nautical miles per voyage, equivalent to roughly $1 million in additional fuel costs and several weeks of additional transit. Algeria’s production is already oriented toward European industrial markets and cannot be rapidly redirected at the semiconductor-grade purity fabs require.

This leaves the United States as the only major alternative supplier — and the US Bureau of Land Management’s Federal Helium Reserve, which had acted as a global price buffer for decades, completed its privatisation in early 2026, removing the backstop precisely at the moment it is most needed. Pricing authority now rests entirely with private operators who have every incentive to maximise margin during a shortage.

Even if Ras Laffan restarts, the problem does not end at the plant gate. Helium containers filled before the strikes are stranded at Ras Laffan with no viable shipping route. The Strait of Hormuz is the only exit. A Cape reroute adds weeks per voyage and approximately $1 million per shipment. If the outage extends beyond two weeks, industrial gas distributors face the additional cost of relocating cryogenic equipment and revalidating supplier relationships — a process that extends months regardless of when Qatari output resumes.

South Korea Is the Blast Radius

The exposure map across semiconductor geographies concentrates acutely in South Korea. Samsung Electronics and SK Hynix together control approximately 70% of the global DRAM market and 80% of the high-bandwidth memory market that powers AI data centres. South Korea imports approximately 65% of its helium from Qatar. For Japan the figure was approximately 64% in 2025. For Taiwan, 69% of imports from GCC states as a whole, per Barclays.

Samsung sits in the highest-risk bracket: its processes are helium-intensive across DRAM, HBM, and advanced logic; its fab-level buffer is estimated at 6–12 weeks; its delivered helium cost in an emergency scenario is 2.0–2.7 times normal. SK Hynix entered the shock with stronger immediate cover — it has publicly confirmed diversified sourcing and additional inventory. TSMC benefits from higher recycling rates (reported 60–75% helium reuse) and a more diversified immediate supply mix, though a quarter of its daily helium losses still require fresh imports. Micron, manufacturing primarily in the US, is the least exposed of the major players.

One critical clarification: industry figures reporting “six months of strategic reserves” for Korean chipmakers are misleading at the operational level. Helium cannot be safely stored in large volumes at fabrication sites. Working inventory at most fabs amounts to approximately one week of supply. Production depends on continuous inbound shipments, not on-site stockpiles. Under normal routing, container transit from the Gulf to South Korea takes approximately one month. Asian fabs continued receiving pre-crisis shipments through approximately early April 2026. After that, the constraint becomes operational. Every wafer start that does not happen in April becomes a memory chip that does not exist in Q3 2026.

“Helium shortages may force chipmakers to prioritise higher-margin AI chips over lower-margin components.”

— Bloomberg Economics analyst Michael Deng, March 2026The downstream effect: NVIDIA, AI hardware, and HDD

TSMC is the sole manufacturer of the logic chips inside NVIDIA’s AI accelerator products. Even a cost increase or modest output reduction at TSMC translates directly into constraints on NVIDIA’s ability to ramp AI products — compounded by the fact that CoWoS advanced packaging capacity was already fully sold out through mid-2026 before this crisis began. On hard drives: every HDD of 10TB and above uses helium as a sealed internal gas, and there is no substitute. Seagate and Western Digital entered 2026 with 20–30% price increases already arriving, and 95% of Western Digital’s HDD output locked to enterprise contracts.

| Company | Country | Primary chips | Qatar He dependency | Buffer (weeks) | Emergency cost (×) | Risk level |

|---|---|---|---|---|---|---|

| Samsung | South Korea | DRAM / HBM / Logic | ~65% | 6–12 | 2.0×–2.7× | Critical |

| SK Hynix | South Korea | DRAM / HBM3E | ~65% | 8–16 | 1.9×–2.6× | High |

| TSMC | Taiwan | Logic / AI chips | ~69% (GCC total) | 10–20 | 1.6×–2.3× | Medium |

| Micron | United States | DRAM / NAND | Low (US domestic) | 12–24 | 1.4×–2.0× | Low |

Bromine, Ethanol, IPA: The Other Materials at Risk

Helium is the acute crisis. It is not the only one. South Korea’s government identified 14 semiconductor supply chain materials with high Middle East exposure in its March 2026 investigation. Bromine, used in circuit formation and chip inspection equipment, is the most critical secondary concern. Approximately two-thirds of global bromine production comes from Israel and Jordan. South Korea sources approximately 90% of its bromine imports from Israel — which is party to the same conflict that has closed Hormuz. Petrochemical-derived chip materials are under indirect pressure from the oil shock itself: thinner (used in photolithography), semiconductor-grade ethanol, and IPA are all tied to crude and naphtha prices, both of which have surged. South Korean suppliers began issuing double-digit price hike notices in the third week of March.

| Material | Primary chip use | Middle East source | S. Korea exposure | Current risk |

|---|---|---|---|---|

| Helium | Wafer cooling, EUV lithography, leak detection | Qatar (~33% of global supply) | ~65% from Qatar | Critical |

| Bromine | Circuit formation, chip inspection equipment | Israel & Jordan (~67% global) | ~90% from Israel | High risk |

| Thinner (PGME/PGMEA) | Photolithography residue removal | Crude / naphtha derived | Indirect — cost-driven | Elevated |

| Semiconductor-grade ethanol | Wafer cleaning, post-etch residue | Naphtha-derived | Double-digit hikes arriving | Elevated |

| IPA (isopropyl alcohol) | Wafer cleaning | Naphtha-derived | LG Chem key supplier | Elevated |

| Aluminium | Chip packaging, interconnects | Qatar smelters offline | Moderate | Watch |

Three Scenarios, Weighted by Structural Evidence

The scenario model below maps three outcome paths for the helium market through to early 2027, with probability weightings based on current structural conditions rather than political optimism. The single variable that would shift probabilities most dramatically — an authenticated ceasefire and verifiable Hormuz reopening — is not visible in current diplomatic signals. Trump has demanded unconditional Iranian surrender. Iran’s foreign ministry has stated they see no reason to negotiate.

Alternative Suppliers Cannot Close the Shortfall

The United States is the only supplier that can increase its effective contribution on a timeline measured in weeks rather than years — and this comes primarily via rerouting existing supply, not new production. US helium output is already near capacity. Algeria’s production is oriented toward Europe and cannot be rapidly redirected at semiconductor-grade purity. Russia’s Amur Gas Processing Plant has been repeatedly knocked offline by explosions since 2021, and Western sanctions make it inaccessible regardless. New primary production projects in Canada, Tanzania, and Minnesota are years from meaningful output. The chart below shows the honest timeline reality.

“The semiconductor industry is betting its future on sub-3nm chips that require more helium per wafer, at the exact moment global helium supply is becoming less reliable. That’s not a risk factor. That’s a countdown.”

— Kunal Ganglani, helium shortage analysis, March 2026Where Capital Is Moving, and Where It Should

The market is already making its bets. Industrial gas distributors are the most direct beneficiaries of a supply shock. Linde PLC is up 15% year to date against a 3% S&P decline; JPMorgan analyst Jeffrey Zekauskas upgraded the stock specifically citing the helium tightening thesis. Air Products is up 14% YTD; Wells Fargo upgraded it to overweight on the same rationale. Air Liquide, which supplies TSMC and more than 60 semiconductor facilities in Taiwan, sits in an equivalent position. These are the cleanest expressions of the helium disruption thesis at low leverage to the conflict outcome: they benefit from price increases, hold global logistics infrastructure to reroute supply, and carry long-term contracts that insulate them from spot market volatility that hits their customers.

On the semiconductor side, the dispersion of risk creates asymmetry. Micron, with primarily US-based manufacturing and domestic helium access, is the least exposed of the major chipmakers. If a prolonged shortage forces Samsung and SK Hynix into production cuts, Micron gains pricing power in DRAM markets it would not otherwise have. The primary concern for pure semiconductor equity plays is the lag: wafer starts that do not happen in April 2026 become chip shipment misses in Q3 2026 reports. The specific mechanism — a helium-driven production cut rather than a demand collapse — is not yet embedded in sell-side models. NVIDIA’s AI ramp, dependent on both TSMC logic and Samsung/Hynix HBM, deserves more attention than it is receiving.

| Company / Asset | Exposure type | Crisis thesis | Key risk | Posture |

|---|---|---|---|---|

| Linde PLC | Helium distributor | Direct beneficiary of price and scarcity; +15% YTD | Early ceasefire collapses thesis | Constructive |

| Air Products | Helium distributor | Same thesis; +14% YTD; Wells Fargo OW | Gulf operations exposure | Constructive |

| Air Liquide | Distributor + TSMC supplier | Reallocation ability; 60+ Taiwan fabs | Own supply if Gulf ops disrupted | Constructive |

| Micron Technology | Chipmaker — low He exposure | Relative value vs. Korean peers; domestic supply | Macro demand destruction | Relative value |

| Samsung / SK Hynix | Chipmaker — high He exposure | Margin pressure; production risk Q2–Q3 2026 | Protracted shutdown exceeds buffer | Cautious |

| TSMC | Chipmaker — medium He exposure | More resilient; still cost headwinds | AI ramp if HBM constrained at Hynix | Neutral–cautious |

| NVIDIA | AI hardware — indirect exposure | Exposed via TSMC logic + Samsung/Hynix HBM | Blackwell ramp bottleneck | Monitor |

| Seagate / WD | HDD manufacturers | He-sealed HDD price hikes already arriving | Enterprise demand freeze if capex cuts | Neutral |

| Pulsar Helium | Primary He production (early stage) | Minnesota primary He; +323% since Sep 2025 | Pre-revenue; high speculative risk | Speculative |

The Blind Spot That Was Always There

The semiconductor industry has survived three major helium shortages in the past two decades: 2006–2007, 2011–2013, 2018–2020. Each was driven by the same combination — plant outages, demand spikes, and the fragility of having so few sources. After each one, the industry talked seriously about supply chain diversification. After each one, the economics of the status quo reasserted themselves and very little changed.

The CHIPS Act and its European and Asian equivalents are pouring hundreds of billions of dollars into new semiconductor fabrication capacity. Every single new fab will need helium. Not one piece of major legislation on semiconductor supply chain resilience has seriously addressed helium supply security. It appears nowhere in the CHIPS Act’s critical materials provisions. This is precisely the kind of blind spot that looks obvious in hindsight — as obvious as neon, which Russia’s 2022 invasion of Ukraine suddenly revealed as an unhedged single-point dependency for semiconductor manufacturing. We learned that lesson and then repeated the structural mistake with helium.

The USGS estimates the world holds approximately 39.8 billion cubic metres of recoverable helium in geological reservoirs. The resource base is not the constraint. Capital investment and policy prioritisation are the constraints. The current crisis has demonstrated, unmistakably, that helium is not a niche industrial gas. It is a strategic material for every economy that manufactures or depends on advanced chips — which is, at this point, every economy. The question is whether governments and chip executives will still believe that in twelve months, when the memory of Ras Laffan fades and the economics of the status quo once again look comfortable.

The Strait of Hormuz closure has two stories. The first — oil, force majeure, tankers, Brent above $100 — is being told loudly and in real time. The second — helium, fabs, rationing, and memory chips — is quieter, slower, and will prove harder to reverse.

Qatar’s Ras Laffan complex supplied roughly a third of global helium before the first Iranian drone reached it on March 2, 2026. As of March 27, it remains offline with no restart in sight. The spot price has doubled. South Korea’s semiconductor industry — controlling 70% of global DRAM and 80% of AI-grade HBM — sources approximately 65% of its helium from that single complex. The in-transit supply buffer runs out in early April. What happens to wafer starts in April determines chip availability in Q3 2026.

Linde and Air Products are the cleanest expressions of the helium disruption thesis. Micron has structural relative value over Korean memory names. NVIDIA’s AI ramp is more exposed to this supply chain than current sell-side models reflect. And the industry’s habit of treating helium supply security as someone else’s problem is the reason this crisis was always waiting to happen.

Sources: Middle East Forum (March 2026); CNBC Markets (March 10, 19, 27, 2026); Fortune Energy (March 21, 2026); Fitch Ratings (March 2026); Barclays Research; Bain & Company Technology Practice; SemiAnalysis (Ray Wang); Gulf International Forum; GasWorld / Kornbluth Helium Consulting; Tom’s Hardware; TrendForce (March 23, 27, 2026); Resilinc (March 2026); J2 Sourcing; Valuates Reports; OilPrice.com; EE Times; Goldinvest.de; Carra Globe; Whalesbook; Boston Globe (March 21, 2026); USGS; JPMorgan (Zekauskas upgrade); Wells Fargo (Sison upgrade); AInvest; Visual Capitalist (Oct 2025). All data current as of March 27, 2026.

Disclaimer: This article is for informational purposes only and does not constitute investment, financial, or trading advice. All prices and data are sourced from third-party providers and are subject to change. Readers should conduct independent research before making any financial decisions.